Monopolies on the Range

How Cleveland Cliffs is flexing its duopoly muscle.

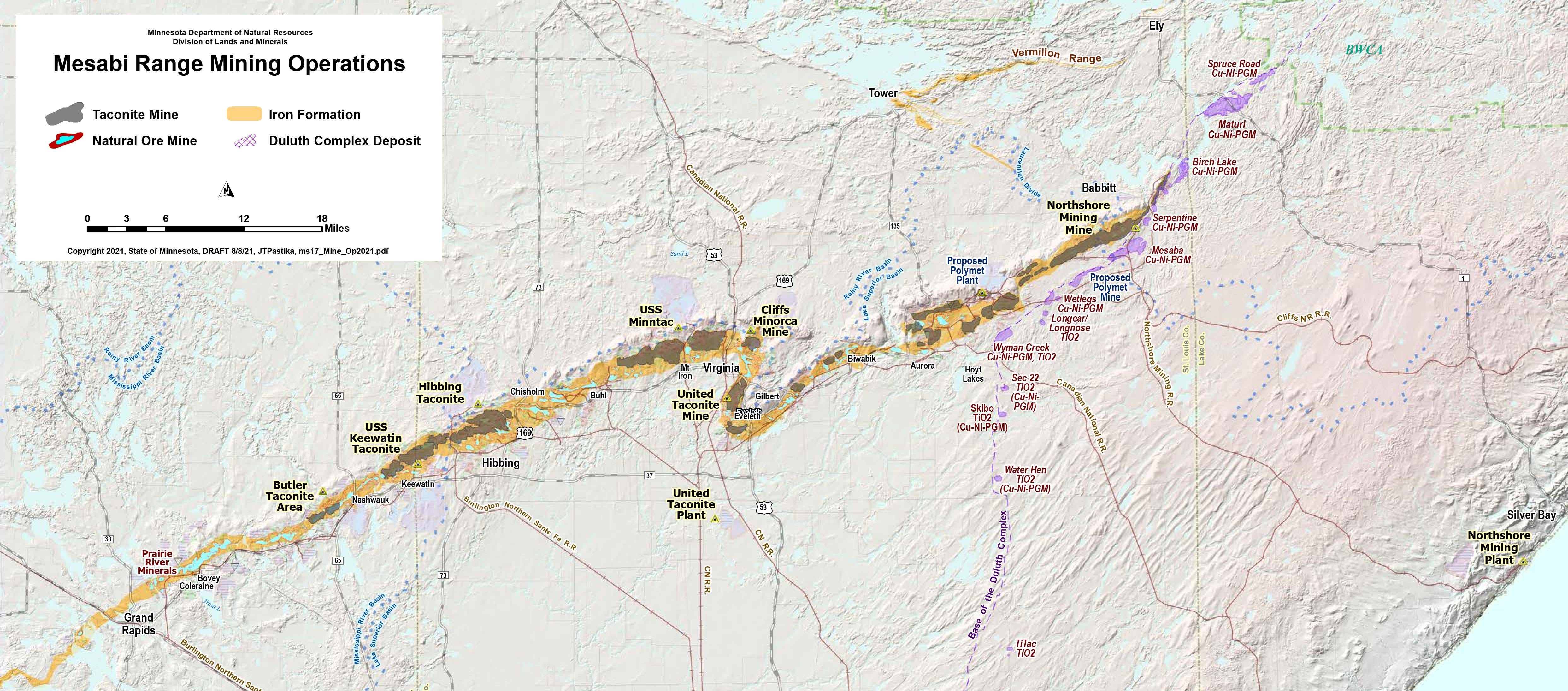

U.S. Steel recently announced it will be investing $150 million in building a new pellet plant at either its Keetac Mine in Keewatin or Minntac Mine in Mountain Iron. The plant will create specialty “DR-grade” pellets that can be used to produce direct reduced iron which is a feedstock for steel mills that use electric arc furnaces, a type of steelmaking that now accounts for more than 70% of steel production in the United States. U.S. Steel has said it could sell the pellets to a third party or use it internally for DRI production in the future.

The U.S. Steel announcement points to where the future of the Iron Range could be headed as domestic steelmakers continue to transition to EAF steelmaking, but it also came on the heels of Cleveland Cliffs announcing earlier in the year that it would be idling its Northshore Mine in Babbitt and its pellet plant in Silver Bay even though Cliffs spent over $100 million in 2019 on capital investments that allow the plant to produce DR-grade pellets. Those pellets supply a new DRI facility in Toledo, OH that opened in 2021.

Cliffs and U.S. Steel control all six (five if you exclude Northshore) of the mines on the Iron Range and Cliffs seems to be using its newfound power to fight a royalty dispute. Unfortunately, it is miners in Minnesota that will bear the brunt of this fight; exposing how monopsony power (the buyer side of monopoly) harms workers, even unionized ones, and the communities they live in.

Cliffs Corner

The Iron Range duopoly is a recent phenomenon. In the 1970s, Minnesota had eight active mines owned by seven different companies. A series of bankruptcies and mergers over the past several decades has left a core economic sector on the Iron Range under the thumb of just two companies, but it is Cliffs that has been engaged in most of the rollup.

Cliffs entered the Iron Range in 1994 when it purchased Northshore Mining. In the early 2000s it took control of United Taconite in Eveleth after its previous owner, Evtac Mining, went bankrupt. Monopolists love nothing more than financial turmoil as a way to consolidate assets. In 2019 and 2020, as the world was turned upside down by the COVID-19 pandemic, Cliffs went about remaking the steel industry in one fell swoop. The company acquired AK Steel in 2019 and ArcelorMittal’s U.S. operations in 2020.

The Arcelor purchase had significant ramifications for Minnesota as it gave the company significant control of jointly-owned Hibbing Taconite, (prior to the merger Arcelor controlled 62.3%, Cliffs 23 percent and US Steel 14.7%) and ownership of the Minorca Mine in Virginia, leaving justCliffs and US Steel to divvy up the Range. The two mergers were a continuation of Cliffs vertical integration. The company entered the scrap steel business in 2021 with the acquisition of Ferrous Processing and Trading Company in Detroit, giving the company control of a key input for its electric arc furnace steel mills.

These transactions have created a steel behemoth. In 2019 Cliffs had revenues of $2 billion and by 2021 that had grown 10-fold to over $20 billion in 2021, with a record profit of over $5 billion last year. Yet despite all that growth and profit, over 400 workers in Babbitt and Silver Bay are now without jobs.

Royalty Fight

After significant capital investments and record profits, why would Cliffs shutter a mine and pellet plant and take on the challenges of transitioning that pellet production to the newly acquired Minorica mine? Monopoly power of course!

More specifically, this is an effort to squeeze Mesabi Trust. Mesabi has a royalty trust agreement in place requiring Cliffs pay Mesabi based on the volume of shipments from Northshore, the price of taconite and the amount of taconite that was mined at Northshore. The royalty structure has been in place since 1989, but it is only now that Cliffs seems to have taken issue with it as CEO Lourenco Goncalves used earnings calls in late 2021 and early 2022 to call the royalty structure ridiculous. Mesabi says Cliffs has never approached them about renegotiating the terms of the royalty agreement and in fact had not informed the company of its plans to idle Northshore.

Caught in the middle of this investor battle are miners who only have two choices, the company that laid them off or U.S. Steel.

History Repeating Itself

Miners on the range have been under the thumb of monopolists before. In the late 1890s oil monopolist John D. Rockefeller took control of Lake Superior Consolidated Mines from the Merritt family in the wake of the 1893 financial crisis (sound familiar?). This gave him control of much of the Iron Range’s mines along with railroad assets. That was just the beginning of the consolidation though, as several years later JP Morgan’s U.S. Steel rolled up Rockefeller’s iron ore and shipping interests along with Andrew Carnegie’s steel assets into a new behemoth.

Like today, workers bore the brunt of Morgan’s new power. Miners were paid not for hours worked, but through a contract system that invited corruption and kickbacks among foreman and workers. Employee safety was an afterthought, as between 1905 and 1910 an average of five out of every 1,000 miners in Minnesota died. More suffered crippling injuries such as lost limbs.

Worker safety and wages for Minnesota miners has improved since the early 1900s, but the recent actions of Cleveland Cliffs underscore that monopoly power is not just bad for competitors, it is bad for workers whether they have the protection of a labor union or not.